Finance

How to Build an Emergency Fund from Scratch

A few years ago, I was sitting on my living room couch, enjoying a quiet Friday evening, when I heard...

•7 minutes read

When I was 23, I decided it was time to become a "grown-up" and start investing. I opened a brokerage account, transferred $500 of my hard-earned savings, and promptly bought shares of a trendy tech company I saw everyone hyping up on internet forums.

Within four days, the stock dropped 30%.

Panicked, stressed, and feeling like I had just been robbed, I sold everything, took my remaining $350, and swore off the stock market entirely. I convinced myself that investing was just legalized gambling for rich guys who wore suits and spoke fluent math.

It took me years to realize that I hadn’t actually been investing—I had been day-trading on pure hype.

Real investing is remarkably boring. It doesn't involve staring at flashing red and green tickers all day, and it doesn't require a degree in finance. Once I stopped trying to outsmart the market and adopted a simple, automated system, my portfolio finally started to grow.

If you are currently sitting on the sidelines because the world of stocks, bonds, and index funds feels completely alien, let’s demystify it together. Here is a step-by-step guide to investing for beginners, written by someone who learned every single lesson the hard way.

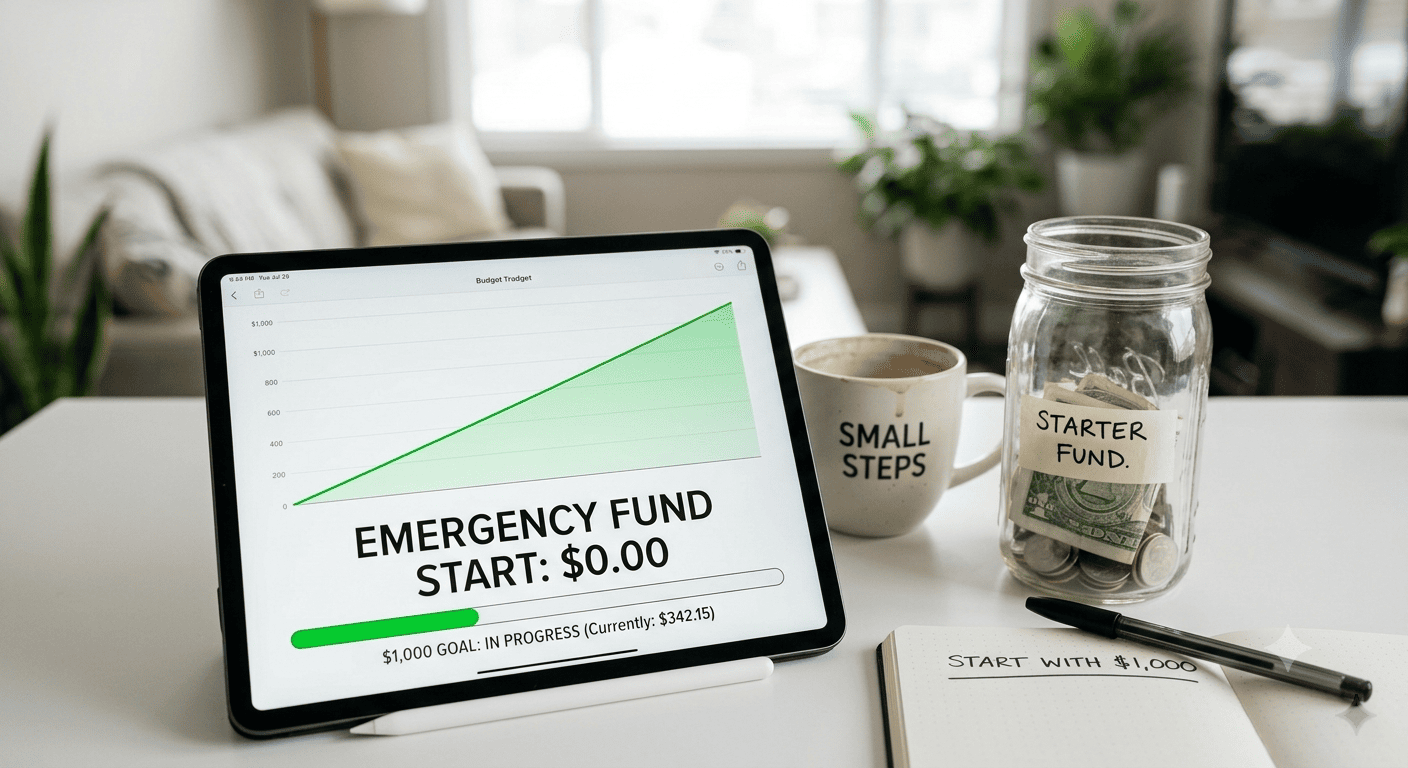

Before you drop a single dollar into the market, you need to make sure your financial house isn't on fire. If you skip this step, an unexpected bump in the road will force you to sell your investments at a loss, just like I did.

Pay down high-interest debt: If you have credit card debt carrying a 22% interest rate, paying it off gives you a guaranteed 22% return on your money. No investment in the stock market can reliably beat that. Clear the cards first.

Build a small buffer: Ensure you have at least $1,000—ideally three to six months of living expenses—tucked away in a high-yield savings account (HYSA). This cash is your shield; it ensures you never have to touch your long-term investments to cover a medical bill or a car repair.

Think of investing like a road trip. Your money is the passenger, the stock market is the destination, and the brokerage account is the car you drive to get there. Different cars have different tax rules.

If your goal is to buy a house in 30 years or retire comfortably, you want a tax-advantaged account.

401(k) or 403(b): If your employer offers this and matches your contributions, start here. If they match up to 4%, contribute 4%. Failing to do this is passing up free money.

Roth IRA: This is my absolute favorite financial tool. You contribute money that has already been taxed, but your investments grow completely tax-free. When you withdraw the money in retirement, you don't owe the government a single penny. Platforms like Vanguard, Fidelity, and Charles Schwab let you open one in ten minutes.

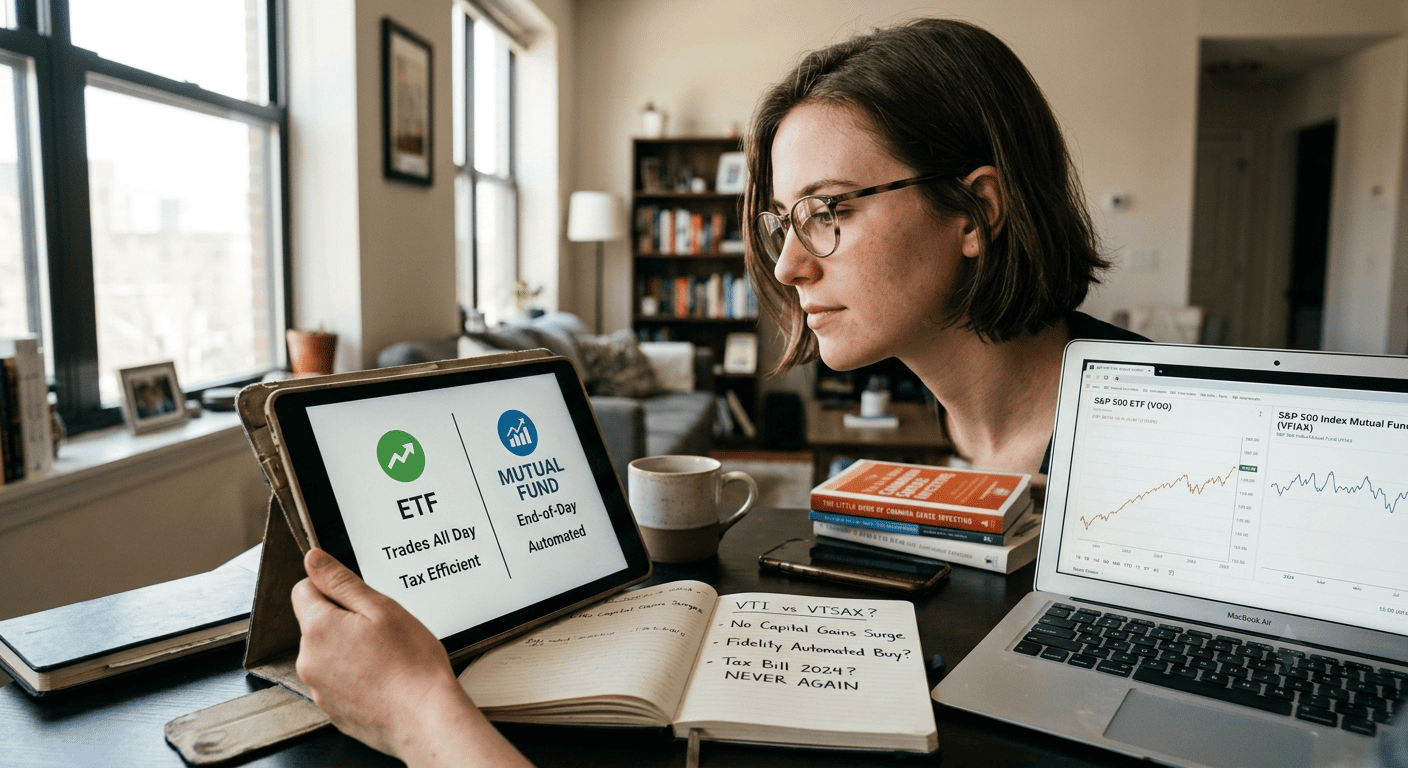

If you want to access your money before retirement (say, you're saving for a major life goal 5 to 10 years out), you want a regular taxable brokerage account. You don't get special tax breaks, but you can withdraw your cash whenever you want without penalties. Apps like Robinhood or Wealthfront make this incredibly user-friendly for beginners.

There are two ways to navigate the stock market: you can try to pick individual winning stocks (Active), or you can buy a tiny slice of the entire market all at once (Passive).

Take it from my $150 mistake: pick passive investing.

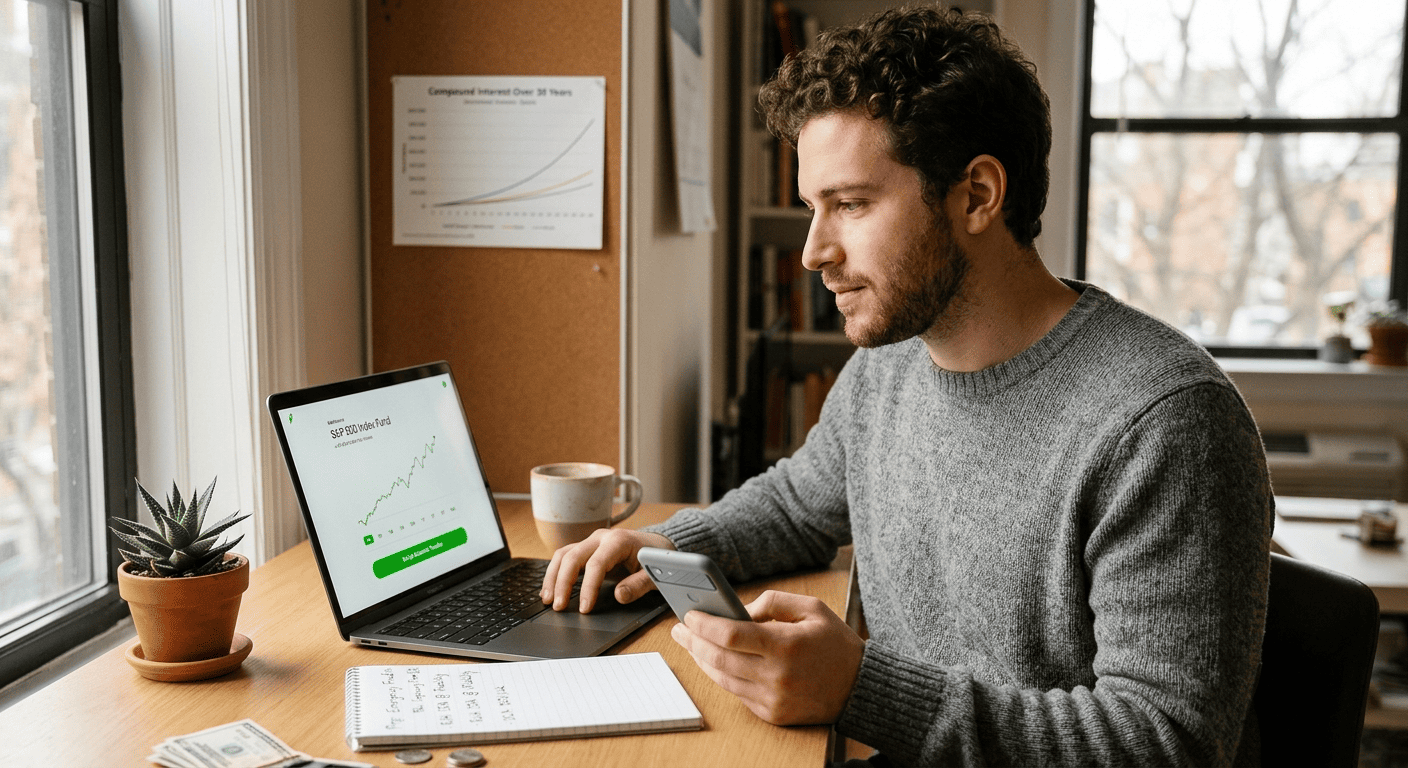

Instead of trying to figure out if Apple, Tesla, or Netflix will perform better next month, you can buy an Index Fund or an ETF (Exchange-Traded Fund).

Think of an individual stock like buying a single piece of fruit. If that specific apple is rotten, you lose your money. An index fund is like buying a massive fruit basket that contains 500 different fruits. If three of them are bad, it doesn't matter because the other 497 fruits keep the basket valuable.

An S&P 500 index fund (like VOO or SPY) buys you a tiny piece of the 500 largest publicly traded companies in America. When the US economy grows over time, your portfolio grows with it. It’s simple, low-cost, and historically beats the vast majority of professional investors over the long haul.

The biggest enemy to your investment portfolio isn't market volatility; it's your own brain. When the market goes down, human instinct screams at us to stop investing and hide our cash under the mattress. When the market goes up, greed tells us to dump all our money in at the absolute peak.

To survive your own emotions, use a strategy called Dollar-Cost Averaging (DCA), which is just a fancy way of saying "automate it."

Set up your brokerage account to automatically buy a set amount of an index fund every single week or month. For example, configure it to buy $50 of an S&P 500 ETF every Friday morning.

When the market is up, your $50 buys fewer shares.

When the market crashes, your $50 goes on sale and buys more shares.

Over time, your purchase price averages out beautifully, and you never have to spend a single second trying to "time" the market perfectly.

Let’s look at two friends, Chris and Maya, to understand why starting early matters so much more than how much money you have.

[ Chris Starts at Age 22 ] ────────────────► Saves $100/mo for 10 Years ──► Stops at 32

│

Grows to: ~$280,000 at age 62

[ Maya Starts at Age 32 ] ────────────────► Saves $100/mo for 30 Years ──► Stops at 62

│

Grows to: ~$160,000 at age 62

Chris invests $100 a month starting at age 22. He does this for just 10 years and stops completely at age 32, never adding another dime. He invested a total of $12,000.

Maya waits until age 32 to start. She invests that same $100 a month for 30 years straight until she turns 62. She invested a total of $36,000.

Assuming a standard 8% average annual return, Chris ends up with significantly more money than Maya at age 62, despite investing a third of the cash.

Why? Because Chris gave his money an extra ten years to experience compound interest. Compound interest is when your money earns interest, and then that interest earns interest, snowballing into a massive mountain of cash over time. Time is the ultimate lever in wealth creation.

When you start playing with real money, pitfalls are everywhere. Keep these rules posted on your wall:

Checking your account daily: Your portfolio will go up and down every single week. Checking it constantly is a surefire way to induce anxiety and make an emotional, irrational trade. Check it once a quarter or once a year.

Chasing the "Next Big Thing": If a coworker, YouTuber, or social media influencer tells you about a cryptocurrency or a stock that is "guaranteed to go to the moon," run away. By the time the general public is hyping it up, the smart money has already left.

Forgetting about expense ratios: Index funds charge a tiny management fee called an expense ratio. Look for funds with fees below 0.1%. Some premium, actively managed funds charge 1% or 2%, which sounds small but will quietly eat up tens of thousands of dollars of your gains over a few decades.

If you have read this far, you have all the theoretical knowledge you need. Now it’s time to take action.

Pick an app: Download an app from an established brokerage firm (like Fidelity, Vanguard, or Robinhood).

Link your account: Link your everyday checking account.

Set up an auto-deposit: Choose an amount that won't strain your daily life—even $10 or $20 a week is a fantastic start.

Buy a broad index fund: Search for a total stock market fund (like VTI) or an S&P 500 fund (like VOO) and set it to auto-buy.

Investing isn't about being rich; it's about buying back your future time. The best time to start investing was ten years ago. The second best time is today. Keep it simple, leave it alone, and let time do the heavy lifting for you.

A few years ago, I was sitting on my living room couch, enjoying a quiet Friday evening, when I heard...

•7 minutes read

Early in my investing journey, I felt like a financial genius. I had set up an automatic monthly transfer into...

•7 minutes read

I used to treat budgeting like a crash diet. Every January, filled with intense financial regret from the holiday season,...

•6 minutes read