Finance

How to Build an Emergency Fund from Scratch

A few years ago, I was sitting on my living room couch, enjoying a quiet Friday evening, when I heard...

•7 minutes read

Early in my investing journey, I felt like a financial genius. I had set up an automatic monthly transfer into a reputable S&P 500 mutual fund through my brokerage account. Every month, like clockwork, it bought shares, and I watched the balance slowly creep upward. I felt completely in control.

Then came mid-April of the following year.

I opened my tax software, imported my documents, and was hit with a completely unexpected tax bill for hundreds of dollars on that exact account. I hadn't sold a single share of my mutual fund. I hadn't cashed out a dime. Yet, I was being forced to pay capital gains taxes simply because other investors in the fund had panicked and sold their shares, forcing the fund manager to liquidate stocks inside the portfolio.

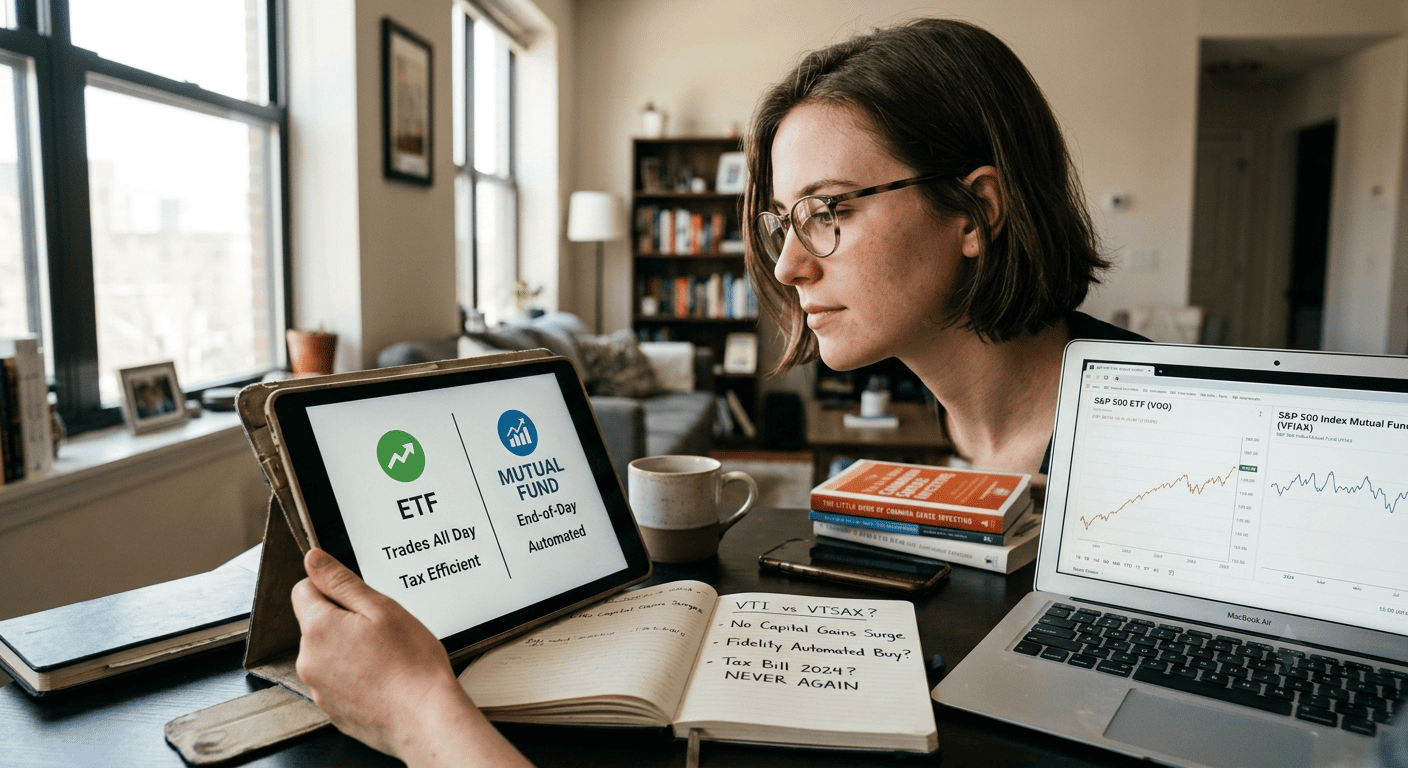

That painful, frustrating tax bill was my introduction to the structural differences between Exchange-Traded Funds (ETFs) and Mutual Funds.

For long-term investors, picking between these two isn't just a matter of semantics. While they can hold the exact same underlying assets, the way they trade, their fee structures, and how they handle taxes can drastically impact your net wealth over ten, twenty, or thirty years. Let’s break down how they actually work in the real world so you can keep more money in your account and less in the hands of the IRS.

To understand the difference, ignore the complex financial jargon. Imagine you want to buy a massive basket of 500 different corporate stocks to diversify your portfolio.

A Mutual Fund is like ordering a custom meal at a sit-down restaurant. You place your order directly with the kitchen (the fund manager) at the end of the day. Everyone pays the exact same price based on the final closing value of the ingredients (the Net Asset Value, or NAV). If you want to leave the restaurant, the kitchen has to physically buy back your meal.

An ETF is like buying a pre-packaged meal from a vending machine on the street corner. It trades on the open stock exchange all day long, exactly like an individual stock. You can buy it at 10:00 AM, sell it at 2:00 PM, and the price fluctuates every single second based on real-time demand.

Because of these architectural differences, each vehicle serves a completely different type of long-term strategy.

For the vast majority of retail investors building wealth in a standard taxable brokerage account, ETFs have become the undisputed heavyweight champion. Here is why:

Remember my painful April tax surprise? ETFs virtually eliminate that issue.

When people want to sell their shares of an ETF, they don't sell them back to the fund manager. They sell them to another everyday investor on the stock exchange. The underlying stocks inside the ETF basket remain untouched, meaning no internal capital gains are triggered for the rest of the group.

Even when an ETF manager does need to adjust the portfolio, they use a highly specialized "in-kind" creation and redemption mechanism with institutional middlemen. This loop functions as a legal tax shield, allowing the fund to avoid realizing capital gains. You only owe capital gains taxes when you choose to sell your ETF shares for a profit.

Because ETFs don't have to deal with the administrative nightmare of managing thousands of individual investor accounts directly, they are significantly cheaper to run.

Mutual funds frequently carry higher "expense ratios" and sometimes sneak in "12b-1 fees"—which are essentially marketing and distribution fees passed directly down to you. While index mutual fund costs have dropped over the years, broad index ETFs regularly boast incredibly low expense ratios, often dipping to 0.03% or 0.04%.

Many institutional or high-quality index mutual funds require a minimum initial investment just to open the door—sometimes $1,000, $3,000, or even more.

With ETFs, the minimum investment is simply the price of a single share. And with modern brokerages like Fidelity, Schwab, or Robinhood offering fractional share trading, you can start investing in a premium ETF with as little as $1 to $5.

Despite the massive surge in ETF popularity, mutual funds aren't dead weight. They possess one hidden superpower that makes them incredibly effective for specific long-term habits.

Because mutual funds are processed directly by the fund company at the end of the day, they allow for absolute, seamless dollar-based automation.

If you want to set up your account to automatically transfer exactly $137.50 from your paycheck every single Tuesday directly into a mutual fund, it will buy exactly $137.50 worth of shares down to the fractional decimal point.

While many brokerages now offer automated recurring purchases for ETFs, traditional mutual funds pioneered this "set-it-and-forget-it" mental framework. There are no bid-ask spreads to worry about, no market hours to track, and no temptation to day-trade because you can't see the price bouncing around during lunchtime.

Furthermore, if you are investing inside a workplace 401(k) or 403(b) plan, you often don't have a choice. These plans are almost universally built on institutional mutual fund share classes, which frequently offer ultra-low expense ratios that compete directly with the cheapest ETFs.

Before you convert your entire financial life to ETFs, you need to understand the concept of asset location.

The primary advantage of an ETF is its protection against annual capital gains distributions. However, inside a tax-advantaged retirement account—like a Roth IRA or a traditional 401(k)—capital gains distributions do not matter. You don't pay taxes on investment growth inside these accounts anyway.

[ Where Are You Investing? ]

│

┌─────────────┴─────────────┐

▼ ▼

[ Taxable Brokerage ] [ Tax-Advantaged Account ]

(Standard Account) (Roth IRA, Traditional 401k)

│ │

Winner: ETFs It's a Tie!

(Saves you from unexpected (Pick based purely on fees

annual tax drags) and automation features)

If you are building your wealth inside a Roth IRA, a low-cost index mutual fund and a low-cost index ETF tracking the same benchmark are essentially a tie. Pick whichever one makes it easier for you to automate your monthly contributions.

Buying Actively Managed Outperformance: Avoid mutual funds or ETFs that charge high fees (anything above 0.50%) under the promise that a professional manager will beat the market. Over a 20-year horizon, the vast majority of active managers lose to simple, low-cost index funds. You end up paying a premium for underperformance.

Ignoring the Bid-Ask Spread on Niche ETFs: Because ETFs trade like stocks, they are subject to a "bid-ask spread"—the difference between the buying price and the selling price. For massive funds like the Vanguard Total Stock Market ETF (VTI), the spread is a fraction of a penny. But if you buy highly specialized, low-volume thematic ETFs, a wide spread can quietly eat into your cash the moment you buy in.

Trading ETFs Out of Boredom: The fact that ETFs can be bought and sold instantly on your phone is a double-edged sword. It makes it incredibly tempting to panic-sell during a market correction or try to time the market. If you choose ETFs, treat them with the same long-term respect as a locked mutual fund.

If you have cash sitting on the sidelines today and need to pull the trigger, follow this direct priority path:

Check the Account Type: If you are investing in a regular, taxable brokerage account, buy the ETF. The tax protection alone makes it the superior vehicle over a long horizon.

Evaluate Your Automation Habits: If you lack the discipline to manually purchase shares and prefer a completely invisible system that pulls money from your checking account to buy exact dollar amounts, look for a no-load index mutual fund inside your retirement accounts.

Compare the Expense Ratios: Open the prospectus or search the ticker symbol on a site like Morningstar. Look at the line titled "Expense Ratio". If the ETF version charges 0.03% and the mutual fund version charges 0.45% for the exact same index, choose the ETF every single time.

At the end of the day, remember that the asset class matters infinitely more than the structural wrapper. Buying a broad-market index fund that exposes you to the compounding growth of the global economy is 95% of the battle.

Whether you choose an ETF or a Mutual Fund, the absolute best thing you can do for your long-term financial health is to pick low-cost options, automate your contributions, and leave the money alone to compound for decades. Don't let the small details paralyze you—pick your vehicle, set up your system, and let time build your wealth.

A few years ago, I was sitting on my living room couch, enjoying a quiet Friday evening, when I heard...

•7 minutes read

When I was 23, I decided it was time to become a "grown-up" and start investing. I opened a brokerage...

•6 minutes read

I used to treat budgeting like a crash diet. Every January, filled with intense financial regret from the holiday season,...

•6 minutes read